Asset financing alternatives and tax considerations

There are various forms of equipment financing and rental solutions available to acquire assets for your business, including operating or finance leases, loans (chattel mortgages) and commercial hire purchase arrangements.

While financing is available for new equipment, these alternatives are also available in the context of a sale and leaseback of existing equipment you own.

Each type of finance will have different commercial features and provide different degrees of asset ownership and impact on cashflow which need to be compared for each alternative. In doing so, there are a number of income tax and GST considerations which need to be considered and taken into account in any cash flow planning when assessing the merits of asset financing.

Loans and operating leases

From an income tax perspective, the treatment of loans (chattel mortgages) and operating leases is fairly simple and easy enough to get your head around. For loans, tax deductions can be claimed by the borrower for interest payments and for operating leases, deductions claimed for lease payments. GST can also be claimed by the lessee on the lease payments.

Hire purchase arrangements

Commercial hire-purchase arrangements can be more interesting. Here, title to the equipment is transferred to the lessee (hirer) at the end of the lease term (on payment of a balloon payment or after an early payout of the lease if applicable).

For income tax purposes, a hire purchase agreement is treated as a sale of the equipment from the lessor to the lessee, combined with a loan. The lessee will therefore generally claim tax deductions for the notional 'interest' component of instalments as well as tax depreciation on the asset (or the upfront tax write off under the temporary full expensing measures). This is contrast with a deduction claimed for the annual total cash lease payments made as would otherwise be the case under a vanilla operating lease structure.

Lessees under hire purchase arrangements who are otherwise able to claim tax depreciation on the assets can get access to the upfront tax write-off under the temporary full expensing measures (assuming all other eligibility criteria are satisfied). This upfront tax benefit should be taken into account in cash-flow planning when choosing the right asset financing solution for your business.

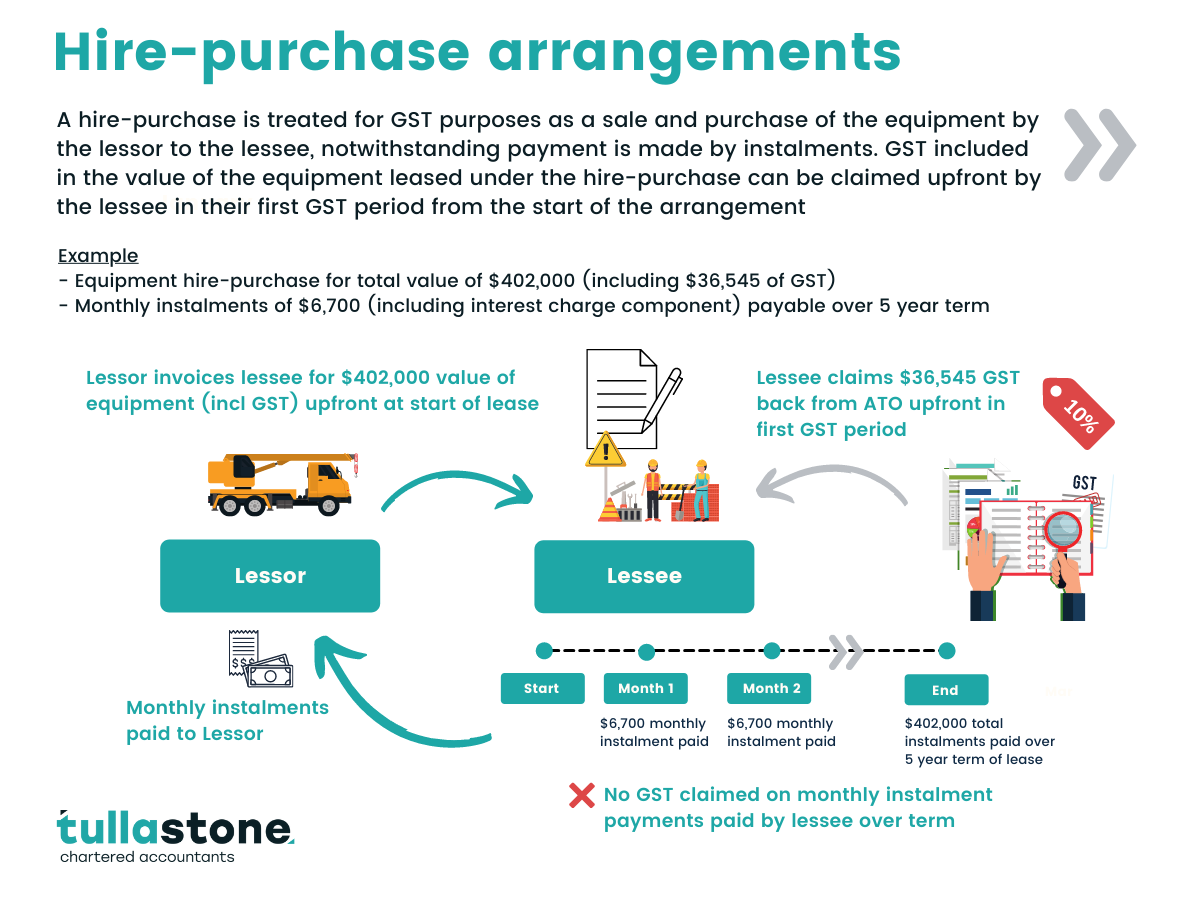

GST and hire purchase arrangements

For GST purposes, a hire purchase is also treated the same as an outright sale and purchase of the equipment at the start of the lease.

For hire purchase arrangements entered into after July 2012, the overall price you pay for the equipment under the hire-purchase will include GST (i.e. including the value attributable to the interest components payable under the instalments).

Lessee's can claim the GST upfront, rather than having to wait until each instalment is paid (regardless of whether they use the cash-basis or accruals-basis for GST accounting). In doing so, the lessee should ensure that a tax invoice is issued to them from the lessor at the start of the hire-purchase arrangement so that the full amount of the GST credit can be claimed.

To the extent the lessor does not require upfront payment of the GST component, then this GST credit can provide a cash-flow boost to the lessee at the start of the lease.

Please reach out to us if you would like more information in relation to these arrangements and to discuss your specific circumstances in more detail.